Automotive Software Market: Transforming the Future of Connected, Autonomous, and Intelligent Mobility by 2034

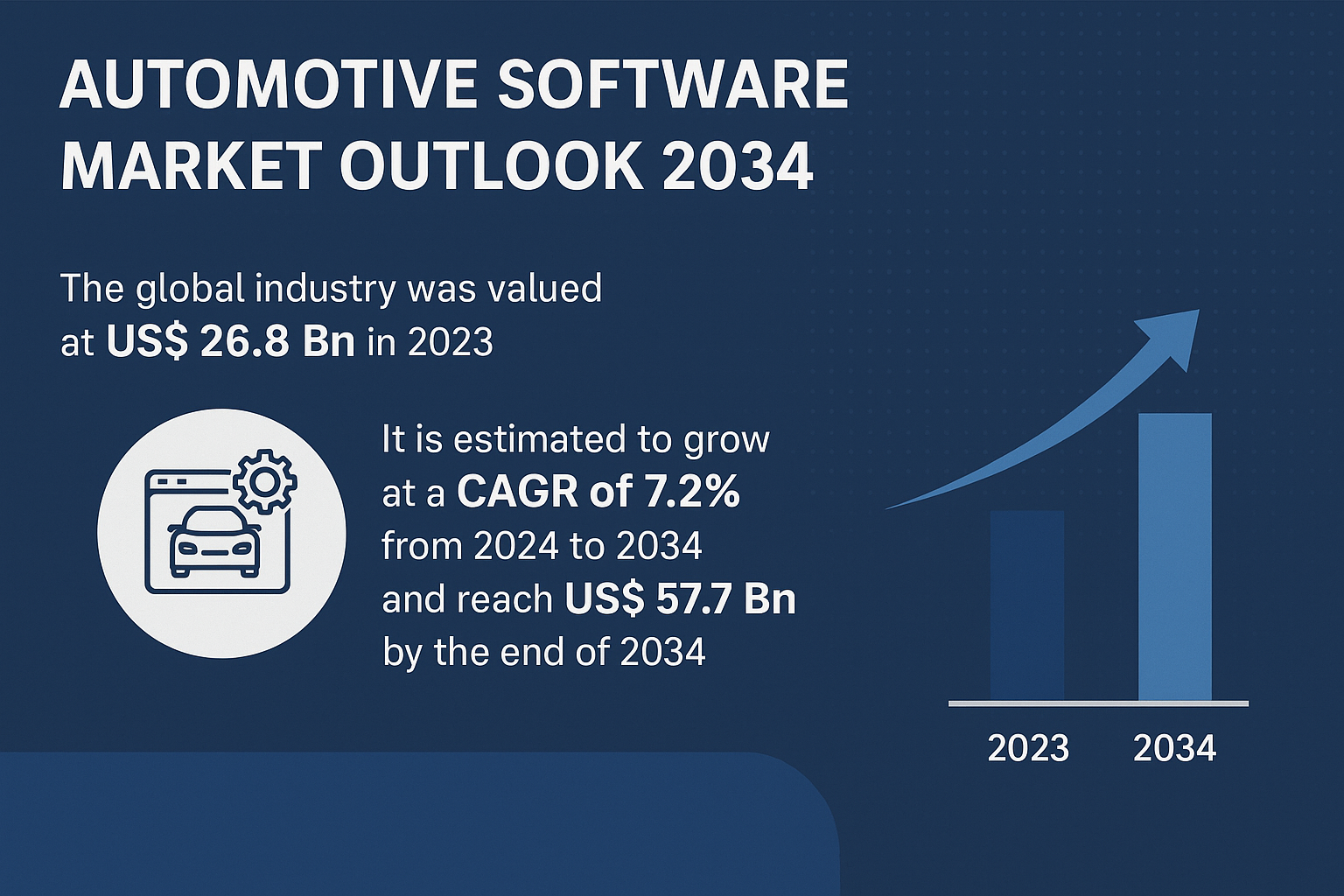

The automotive industry is undergoing one of the most profound transformations in its history, driven by the rapid integration of software across all essential vehicle systems. The Automotive Software Market, valued at US$ 26.8 Bn in 2023, is expected to reach US$ 57.7 Bn by 2034, expanding at a strong CAGR of 7.2%. As vehicles shift from mechanical machines to intelligent, connected, and semi-autonomous platforms, automotive software has emerged as the core enabler of innovation, safety, efficiency, and user experience. This shift is prompting automakers, technology companies, and software developers worldwide to invest heavily in next-generation operating systems, middleware, cloud platforms, simulation tools, and AI-driven mobility solutions.

This in-depth article explores the market landscape, key growth drivers, regional trends, technological advancements, challenges, opportunities, and competitive strategies shaping the global automotive software ecosystem.

Evolving Role of Automotive Software: From Mechanical Systems to Intelligent Platforms

Automotive software has become the backbone of new-generation vehicles, performing real-time data processing, enabling connectivity, and supporting advanced control functions. From ADAS to infotainment, vehicle telematics, powertrain management, and autonomous driving, modern vehicles rely on highly integrated software architectures designed to manage thousands of signals each second.

Today’s automotive software operates at multiple layers:

1. Middleware

Ensuring seamless communication between hardware and application layers while enabling faster deployment of mobility features.

2. Operating Systems

Providing secure, scalable platforms to run critical vehicle functions—from battery management to ADAS computation.

3. Application Software

Enabling user-facing and intelligence-driven features such as navigation, entertainment, safety alerts, remote diagnostics, and cloud connectivity.

The increasing volume of data from sensors, cameras, radar, LiDAR, and telematics devices has made real-time software execution crucial for safe on-road decision-making. As autonomous vehicle development accelerates, the sophistication and importance of automotive software will multiply exponentially.

Key Market Growth Drivers

1. Surge in Adoption of Advanced Technologies in Vehicles

Vehicles are now equipped with smart features that require complex algorithms, edge processing, and intelligent decision-making. Software coordinates all vehicle components—engines, brakes, infotainment systems, and ADAS platforms—leading to enhanced control, efficiency, and safety.

-

More than 1.1 million licensed plug-in vehicles were running in the U.K. as of December 2022.

-

Between April and June 2022, the U.K. registered 79,000 new plug-in vehicles—all equipped with advanced electronic systems.

With the rise of EVs, sensor-based driving assistance systems, and connected vehicles, the need for specialized vehicle operating systems is at an all-time high.

2. Expansion of Automotive Infotainment Systems

Customer expectations for seamless, smartphone-like experiences inside vehicles are driving significant adoption of advanced infotainment platforms.

-

Mitsubishi Motors, Nissan, and Renault have selected Google’s Android OS for upcoming vehicles.

-

Hyundai, Kia, and Genesis models now integrate NVIDIA Drive, demonstrating how AI is becoming central to infotainment innovation.

Consumers increasingly demand navigation guidance, media streaming, digital assistants, smartphone integration, and app-based controls. This shift is fueling robust demand for application software, HMI systems, and cloud-based telematics.

3. Rise in Connected Mobility and IoT Integration

Automotive IoT is enabling predictive maintenance, real-time traffic management, vehicle tracking, and enhanced safety through V2X communication. As regulators push for improved road safety and emissions control, connected mobility solutions are rapidly becoming standard.

4. Development of Autonomous and Semi-autonomous Vehicle Technologies

Autonomous driving requires software-intensive systems that can analyze massive data volumes, detect objects, evaluate scenarios, and respond instantly. High computational power and ML-driven software frameworks are essential in this domain.

Companies are developing integrated platforms that process sensor fusion, trajectory prediction, and driving behavior—all of which depend heavily on software innovation.

Market Segmentation Analysis

The automotive software market is broad, spanning multiple categories:

By Software Layer

-

Middleware

-

Operating Systems

-

Application Software

By Software Type

Includes CAD, CAE, FEA, CFD, Multibody Dynamics, CAM, Telematics, Diagnostic Software, Embedded Software, Vehicle Simulation Software, and more.

By Application

-

ADAS & Safety Systems

-

Body Control & Comfort

-

Infotainment Systems

-

Electric Drive

-

Vehicle Telematics

-

Battery Management

-

Autonomous Driving

-

Charging Management

-

V2X Systems

-

Others

By Offering

-

Solutions

-

Services

By Vehicle Type

From two-wheelers to heavy-duty trucks, buses, off-road vehicles, and agricultural equipment.

By Electric Vehicle Type

-

Battery Electric Vehicles (BEVs)

-

Hybrid/Plug-in Hybrid Electric Vehicles (HEVs/PHEVs)

-

Fuel Cell Electric Vehicles (FCEVs)

By Autonomy Level

-

Autonomous

-

Semi-autonomous

The layered segmentation reflects the depth and complexity of the automotive software ecosystem, which touches every aspect of modern vehicle engineering and mobility technology.

Regional Overview

1. North America: The Global Leader

North America accounted for the largest market share in 2023 due to:

-

Strong automotive production

-

Presence of leading tech giants such as Google, NVIDIA, and Microsoft

-

High demand for connected and autonomous vehicles

-

Early adoption of EVs and smart automotive technologies

The U.S. leads innovation with software-defined vehicle (SDV) architectures and robust investments in ADAS research.

2. Asia Pacific: Fastest Growing Region

Asia Pacific is witnessing explosive growth due to:

-

Market dominance of China in commercial vehicle manufacturing

-

Rapid adoption of advanced features in Japan, China, South Korea, and India

-

Strong EV manufacturing ecosystem

-

Government incentives supporting connected mobility

China produced 3.18 million commercial vehicles in 2022, while Japan produced 1.27 million, showcasing massive potential for software deployment.

3. Europe: Strong Innovator in Automotive Digitalization

Europe remains a major hub for:

-

ADAS development

-

Autonomous driving research

-

Strict regulatory frameworks supporting road safety

-

Integration of digital cockpit technologies

Countries such as Germany, France, the U.K., and Nordic nations are heavily investing in EVs and intelligent transportation systems.

4. Middle East & Africa and South America

While emerging, these regions show rising adoption of telematics, fleet management systems, and connected vehicle technologies driven by logistics and transportation industries.

Key Player Strategies and Competitive Landscape

Leading companies are focusing on AI integration, modular vehicle OS platforms, cybersecurity solutions, and advanced computing architectures. Major players include:

-

Airbiquity Inc.

-

Alphabet Inc.

-

BlackBerry Limited

-

Continental AG

-

DXC Technology

-

Green Hills Software

-

HARMAN International

-

KPIT Technologies

-

Microsoft

-

NVIDIA

-

NXP Semiconductors

-

Robert Bosch GmbH

-

Siemens

-

TomTom

-

Wind River Systems

Strategies Dominating the Market

1. Platform Development for Software-defined Vehicles (SDVs)

Companies are working to standardize software and hardware ecosystems, enabling frequent OTA updates and modular software enhancements.

2. Adoption of AI and Machine Learning

AI-powered software optimizes driving decisions, enhances infotainment experience, and improves battery life in EVs.

3. Partnerships and Collaborations

Notable examples include:

-

NXP Semiconductors and Elektrobit collaboration in 2022 to develop next-gen automotive battery management system software.

-

TTTech Auto secured US$ 285 Mn from Aptiv and Audi to strengthen its safety software platforms for autonomous mobility.

4. Cybersecurity Integration

With increased connectivity comes greater risk. Manufacturers are incorporating strong encryption, intrusion prevention systems, and secure vehicle operating systems to counter cyber threats.

5. Focus on OTA Updates and Cloud-based Services

Real-time software updates enhance performance, fix bugs, and introduce new features without dealership visits.

Market Challenges and Opportunities

Major Challenges

-

High complexity of real-time automotive systems

-

Cybersecurity vulnerabilities

-

Need for universal software standards

-

High development costs for autonomous driving software

-

Shortage of skilled automotive software developers

Opportunities

-

Growth in smart mobility and urban transportation solutions

-

Increasing EV adoption

-

Intelligent cloud-based vehicle management services

-

Expansion of digital cockpits

-

Rise of mobility-as-a-service (MaaS)

-

Government mandates supporting ADAS

As vehicles become more intelligent and autonomous, the demand for scalable, secure, and efficient software will grow exponentially over the next decade.

Future Outlook: A Software-defined Automotive Era

The next decade will transform the automotive ecosystem into a software-defined mobility environment, where software dictates most vehicle features, performance capabilities, and user experiences. The automotive software market will see:

-

Wider adoption of centralized computing architectures

-

Rapid growth in domain and zonal controllers

-

Increased focus on virtual simulations for vehicle testing

-

Massive reliance on AI, deep learning, and edge computing

-

Integration of blockchain-based vehicle security systems

-

Increased use of digital twins for system-level modeling

By 2034, vehicles will essentially be computers on wheels, operating through unified platforms that seamlessly update and evolve over time.